January 17, 2025

Chinese Steel in 2025 | By Zhongmin

In 2025, China’s steel industry will continue to face multiple challenges while also encountering new opportunities. These include the expansion of Belt and Road Initiative partner countries, the gradual implementation of large-scale equipment upgrades and consumer goods trade-in policies, and the expected effects of monetary easing measures introduced during the 2024 Central Economic Work Conference. Key policies such as stabilizing real estate and stock markets, increasing fiscal expenditures, expanding special bond issuances, and potential reserve requirement ratio (RRR) and interest rate cuts are set to take full effect.

Macroeconomic Environment Remains Challenging

Global Economic Growth Slows

The International Monetary Fund (IMF), in its October 2024 World Economic Outlook report, projected a 3.2% global GDP growth rate for 2025, unchanged from 2024. Goldman Sachs, however, forecasts a lower growth rate of 2.7%.

- United States: GDP growth is expected to slow to 2.2% in 2025 (down from 2.8% in 2024).

- Eurozone: A modest recovery is anticipated, with GDP growth rising to 1.2% (from 0.8% in 2024). Germany is also projected to grow at 1.2%.

- Emerging Markets:

- India’s GDP growth is forecast at 6.5%, down from 7% in 2024.

- China’s growth is expected to reach 4.8%.

- Brazil’s growth may dip slightly to 2.2%.

- Japan faces persistent high inflation and monetary policy normalization challenges, with growth estimated at 1%.

- Russia’s growth is projected to drop sharply to 1.5% (from 3.2% in 2024) due to geopolitical strains.

Trade Pressures Intensify

U.S.-China tensions are likely to escalate, with the new U.S. administration expected to impose stricter trade and investment restrictions on China. This could lead to higher tariffs and broader export bans, directly and indirectly affecting China’s steel exports. Additionally, post-Brexit trade negotiations and regional conflicts add further uncertainty to global trade dynamics.

Geopolitical Risks Rise

- The spillover effects of the renewed Israel-Hamas conflict have drawn in Lebanon, Iran, Yemen, and Syria, destabilizing the Middle East.

- Escalating clashes between Pakistan and Taliban militants highlight the region’s fragile security.

- The Russia-Ukraine war enters its fourth year, with Western support for Ukraine prompting a more aggressive stance from Russia, increasing the risk of further escalation.

Demand Recovery and Strong Exports

Global Steel Demand Expected to Improve in 2025

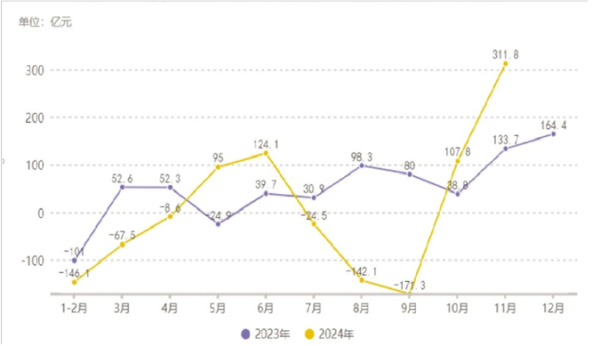

China’s steel industry will continue to grapple with oversupply and weak demand in 2025. According to the National Bureau of Statistics, profits in the ferrous metal smelting and rolling sector plummeted by 80.4% year-on-year in the first 11 months of 2024, totaling just 7.86 billion yuan. Overcapacity remains a key challenge, but falling iron ore prices—driven by increased supply—could ease cost pressures.

The industry has shown signs of recovery since October 2024, returning to profitability (see Figure 1). Overall, global steel demand in 2025 is expected to outperform 2024 levels.

Black Matel Profile in China (2024) 2025 Chinese Steel .